As a result of the global financial crisis, elevated levels of sovereign debt and extremely expansive monetary policies by all major central banks around the world have led to growing concerns about inflation among the investment community. Since 2008, central banks are keeping interest rates low by providing massive liquidity into their economies, whereas the probability of high inflation rates in the future has increased significantly.

Milton Friedman, a well known economist, stated once that “Inflation is always and everywhere a monetary phenomenon.” On Monday (4th March 2014), the five year US inflation expectations rose to their highest level in seven months, as investors are seeking insurance against the prospect that a recovering economy will stoke price pressures.

Basically, inflation is an increase in prices since there is too much money for fewer goods around. However, right now this is not an immediate problem, since the output gap of the U.S. has still a lot room for improvement and unemployment remains elevated, and therefore, the current inflation expectations remain quite low for the time being. Nevertheless, inflation will become a huge issue sooner or later; at the latest, when the economy is getting back on track.

Moreover, if this is the case, interest rates will rise too, and fixed income investors will suffer the most, as bond prices will decline and inflation will wipe out all the earned interest and principal. Even Warren Buffet said recently in an interview that low interest rates and inflation should dissuade investors from buying bonds and other holdings tied to currencies.

In addition, for conservative investors at or near retirement, inflation can be the biggest threat, since at this stage, many of them have converted much of their portfolio into fixed income to protect capital. As a consequence, investors will be in the need of an inflation-proof portfolio, since a heavy loaded bond portfolio won’t be the perfect hedge for such a scenario. Diversifying a portfolio’s income stream with investments that are less affected by inflation is the only way to fight the upcoming inflation threats. Moreover, investors at or near retirement are in the need of a more or less low risk/volatility portfolio that should generate stable returns.

In general, there are enough asset classes around which should provide a good hedge against an inflationary environment:

The main problem with the mentioned asset classes above is the fact that most of them are highly volatile/risky, and therefore, creating a conservative inflation-proof at or near retirement portfolio can be quite challenging.

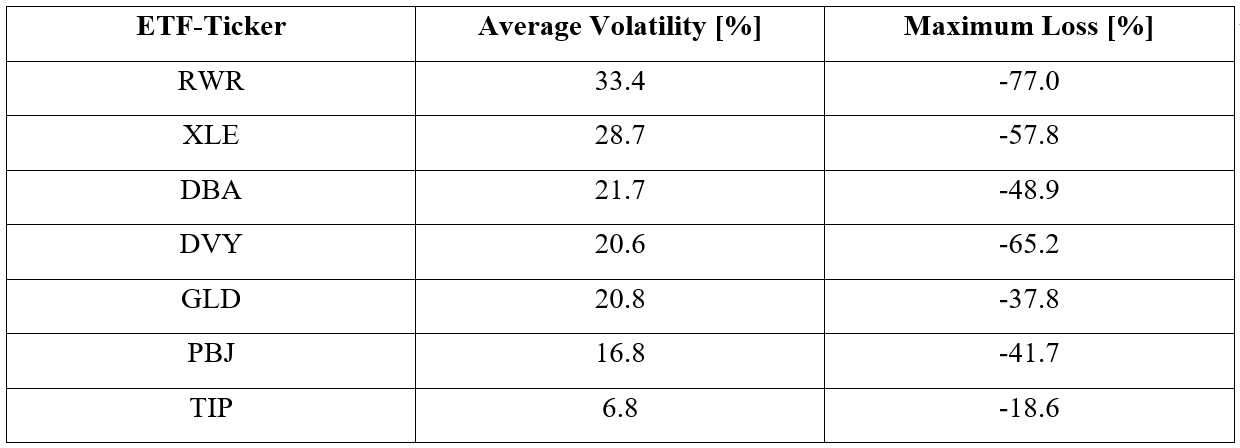

Table 1: Asset Classes and their average volatility and maximum loss

For that reason, we would like to highlight a conservative inflation-proof model portfolio which is regularly being updated on our website. The main target of the portfolio is to generate enhanced and stable returns above the average inflation rate and to minimize potential losses, even during times when the overall inflation expectations remain quite low. The “Inflation Proof Retirement Portfolio” is constructed by applying the so-called Maximum Diversification approach, which we have already reviewed extensively in previous Seeking Alpha articles. In general, the basic idea behind the maximum diversification approach is to construct a portfolio that maximizes the benefits from diversification.

First of all, diversification can be measured by the so-called diversification factor. This factor is the portfolio’s weighted average asset volatility to its actual volatility. The result of this calculation measures the essence of diversification. For a given set of assets, there is a long-only portfolio solution that maximizes the diversification factor. In other words, if the overall correlation coefficient of any underlying security increases, the less weighting it will receive, since its diversification benefits are decreasing. For that reason, the portfolio is balancing the risk of its underlying asset classes to minimize the overall portfolio volatility, as it is possible to put the maximum weight into each asset class whereas the overall portfolio risk (volatility) is not being increased at all. Theoretically, if the expected returns of the underlying asset classes are perfectly proportional to their total asset risk, there should be no other portfolio combination that can achieve a higher Sharpe Ratio.

As already mentioned above, the Inflation-Proof Retirement Portfolio has the following investment universe:

Apart from the iShares Barclays TIPS Bond (TIP), the investment universe of the Inflation Proof Retirement Portfolio solely consists of non-fixed-income investments. Furthermore, in our example, there is no allowance for transaction costs or brokerage fees. In order to minimize transaction costs, we rebalance the portfolio on a monthly basis.

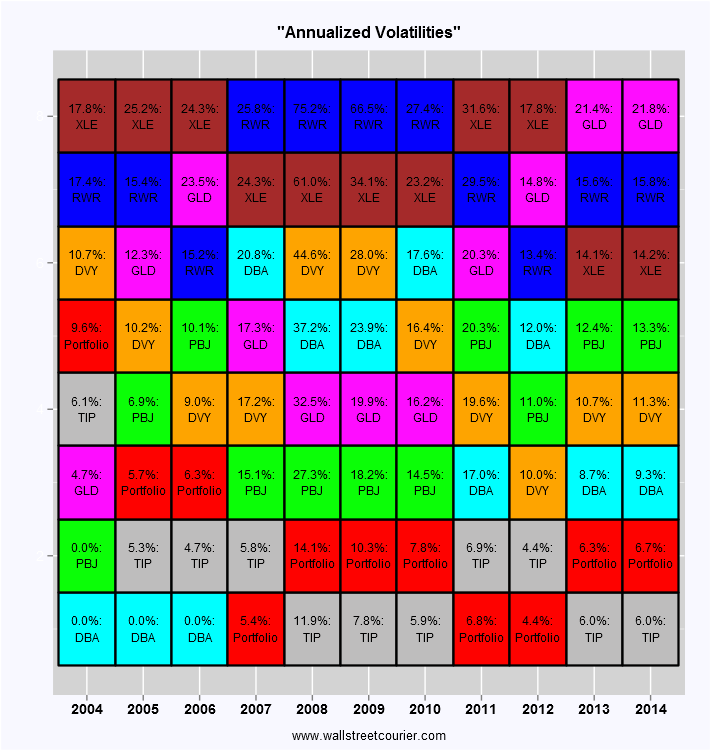

If we have a look at the annualized volatility this portfolio utilized in the past, we can see that apart from 2008, where the financial crisis hit the markets, the portfolio volatility itself swung between 4 and 10 percent. The average volatility, in contrast, was around 8.5 percent, although we are mainly using high volatile asset classes (volatility of zero percent means that the ETF was not available during that time).

Chart 1: Annualized Volatilities

The allocation of the portfolio for January and February can be seen in the table below:

Table 2: Allocation of the Portfolio for January and February

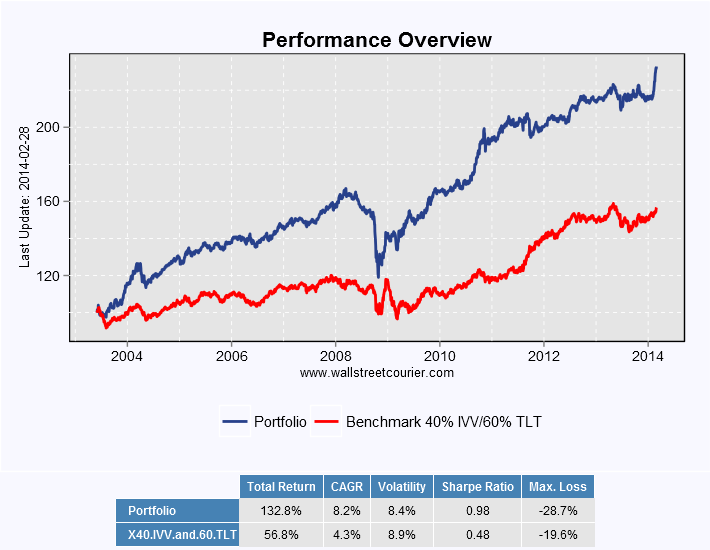

Chart 2: Performance Overview of the Portfolio and the Benchmark

Due to its high diversification benefits, the portfolio almost achieved a Sharpe Ratio of 1, indicating that investors have received 1 percent performance for each unit of risk. This is mainly due to the fact that it is possible to put the maximum weight on each asset class without increasing the overall portfolio volatility.

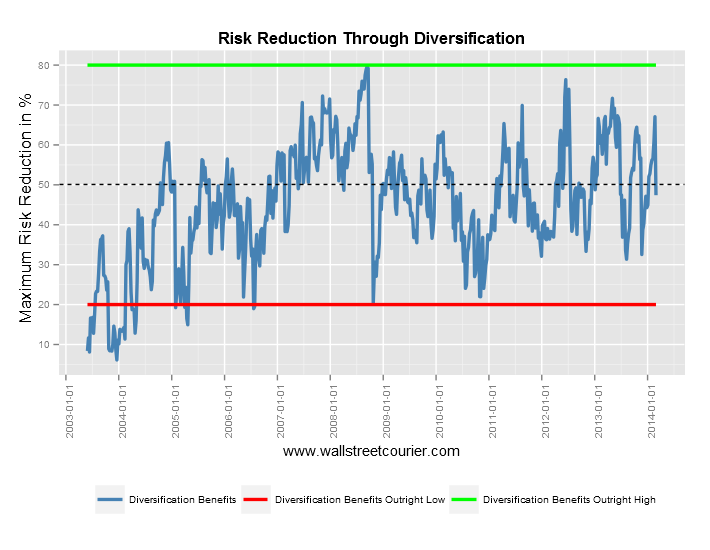

To visualize this effect, we have plotted a ratio which measures how much risk-reduction in percent the portfolio utilizes through diversification. For example, if the portfolio’s weighted average asset volatility is 20 percent and the actual portfolio volatility itself is only 4 percent, the ratio reaches a score of 80 percent. This means that the portfolio only carries 20 percent of its initial risk.

In such an environment, nearly all underlying asset classes are perfectly uncorrelated to each other and, therefore a draw-down in any underlying asset class does not have a big impact on the overall portfolio performance. The case is different if the ratio drops near or even below 20 percent, indicating that most asset classes are highly correlated to each other. In such an environment, risk reduction through diversification is not working very well, since even a perfect diversified portfolio still carries 80 percent risk from its underlying asset classes. Such a fact is not really a big threat for a diversified portfolio, as long as the overall momentum of the underlying asset classes remains positive. Large draw-downs are only occurring if the ratio drops below or near 20 percent and if simultaneously all asset allocated classes are facing strong declines (e.g. 2008).

Chart 3: Risk Reduction Through Diversification

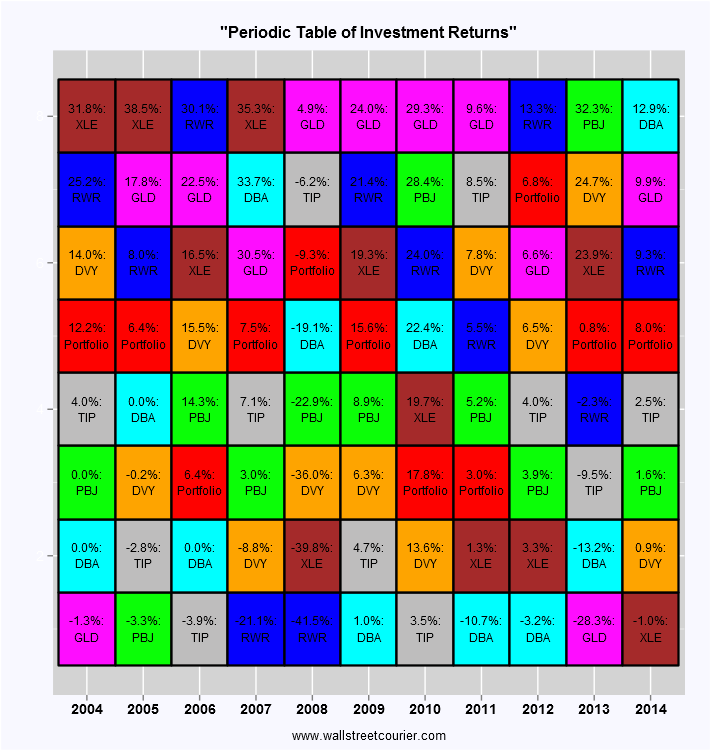

Another interesting fact is to look at the Callan periodic table of investment returns, where the yearly returns of each underlying asset classes and of the portfolio itself are plotted in descend ending order. There we can see that the portfolio is achieving quite attractive results, especially if we consider the fact that the historical annualized volatility of the portfolio was extremely low.

Chart 4: Periodic Table of Investment Returns

The portfolio is designed to generate stable returns during all predominant market conditions, even if the inflation expectations remain low. For that reason, such a portfolio is a perfect solution or complement investment for investors at or near retirement who are searching for a conservative inflation-proof investment which is not heavily loaded on bonds.

Author: Robert C. Koch

Note: This research publication was published on Seeking Alpha in March 2014.

© 2023 WallStreetCourier – Identifying Profitable Market Regimes since 1999.